GRACE Methodology

A governance methodology developed by Andrew Young.

The GRACE Framework provides a structured methodology for analysing whether modern large-scale public policy systems remain lawful, fiscally sustainable, operationally deliverable and subject to democratic scrutiny

The methodology is analytical rather than prescriptive; it applies structured governance tests to examine public policy systems rather than prescribing specific policy outcomes.

The methodology itself does not require legislative change. However, when applied to real policy environments, the analysis generated through the framework may identify areas where legislative or institutional reform would be appropriate. Any such proposals arise from the policy analysis produced using the framework rather than from the methodology itself.

The methodology presented on this page provides an overview of the principal operational components of the GRACE Framework. It should be understood as part of a wider constitutional governance discipline in which governance assessment, evidence, assurance and continuous institutional learning operate together to support transparent, accountable and resilient public administration.

Introduction

The GRACE Framework is built around a structured governance methodology designed to examine complex public policy systems in a transparent and auditable way.

Rather than relying solely on narrative policy proposals, the framework introduces structured decision gates and reconciliation controls that test whether policy systems remain lawful, fiscally bounded, operationally deliverable and subject to democratic scrutiny.

In practical terms, the methodology examines public decision-making across the full lifecycle of governance:

authority → legality → cost → delivery → risk → outcomes

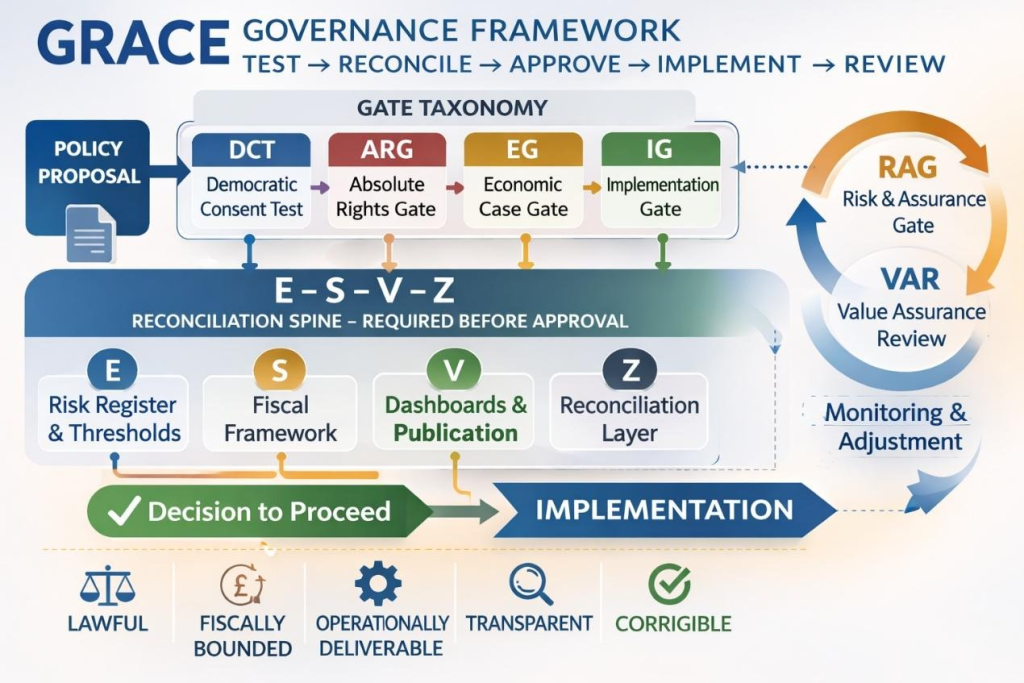

Figure — GRACE Governance Architecture

Policy proposals pass through governance gates and reconciliation checks before implementation, with continuous monitoring throughout the policy lifecycle

The Gate Taxonomy provides the structured checkpoints through which these governance tests are applied both at the proposal stage and throughout the operational lifecycle of a policy system.

The GRACE Framework therefore operates not merely as a policy proposal but as a structured methodology for examining whether complex public systems remain lawful, fiscally bounded, operationally deliverable and subject to democratic scrutiny over time.

Gate Taxonomy

The GRACE methodology uses a Gate Taxonomy to define discrete decision checkpoints within a policy system. Each gate tests a different aspect of governance. A proposal can only proceed if it satisfies the requirements of the relevant gate.

Gate Structure

| Gate | What it Tests |

| DCT — Democratic Consent Test | Has the proposal been clearly explained with defined authority, scope and cost? |

| ARG — Absolute Rights Gate | Would the proposal breach non-derogable legal or safeguarding protections? |

| EG — Economic Case Gate | Is the proposal fiscally credible and transparently funded? |

| IG — Implementation Gate | Is the system operationally ready and capable of safe delivery? |

| RAG — Risk & Assurance Decision Gate | Are risks monitored with defined escalation and correction mechanisms? |

| VAR — Value Assurance Review | Is the system delivering the intended outcomes over time? |

The gates operate cumulatively. Passing one gate cannot compensate for failure at another. Their purpose is not to slow decision-making but to help ensure that public systems remain lawful, bounded and corrigible.

Within the GRACE methodology, governance gates operate as structured decision checkpoints supported by evidence-based due diligence. Proposals passing through these gates would normally be accompanied by supporting documentation such as independent assessments, financial analysis, operational reviews, safeguarding reports, or audit evidence. These materials provide the evidential basis upon which governance decisions can be examined.

By requiring independent governance tests supported by verifiable evidence, the GRACE methodology reduces the ability of policy narratives to obscure structural weaknesses within a system. Because each governance gate examines a different dimension of system design — legal authority, fiscal sustainability, operational capacity and risk monitoring — no single narrative or policy argument can compensate for failure in another domain.

In addition, the framework’s reconciliation architecture (E–S–V–Z) links risk registers, fiscal attribution, transparency dashboards and institutional accountability. By connecting these signals across the lifecycle of a policy system, the methodology makes inconsistencies easier to detect and allows external observers— including auditors, journalists, parliamentary committees and researchers — to apply the same governance tests independently.

For this reason, the GRACE Framework does not assume that institutions will always behave perfectly. Instead, it seeks to design governance structures that make narrative distortion, concealment of risk and fragmentation of responsibility more difficult to sustain over time.

GRACE Control Spine (E–S–V–Z)

The Gate Taxonomy operates alongside the GRACE framework’s reconciliation architecture, known as the E–S–V–Z control spine. This structure ensures that risk, fiscal exposure, transparency and institutional accountability remain connected.

| Annex E — Risk Register & Thresholds | Defines risk triggers and escalation thresholds. |

| Annex S — Fiscal Framework | Establishes fiscal attribution, cost controls and financial safeguards. |

| Annex V — Dashboards & Publication Pack | Provides transparency through published indicators and methods. |

| Annex Z — Reconciliation Layer | Connects risk, fiscal exposure and transparency into a structured accountability system. |

GRACE does not override Parliament.

It informs Parliament.

The framework’s role is visibility and accountability, not veto power. Parliamentary institutions remain free to approve or reject policy proposals. The purpose of the framework is to ensure that such decisions are taken with clear visibility of legal constraints, fiscal exposure, operational capacity and systemic risk.

Public systems should not rely on scandal to trigger oversight.

Oversight should be embedded in the design of the system itself.

Complex governance systems rarely fail because of a single decision. More commonly, risks accumulate gradually as multiple policy decisions interact across legal, fiscal and operational domains. When these cumulative effects are not visible, institutions may assume that fiscal capacity or administrative resilience will absorb the pressure.

The GRACE Framework therefore operates as an early-warning architecture for cumulative governance risk. By applying structured decision gates and transparency mechanisms, the framework allows risks to become visible before they escalate into systemic failure or uncontrolled fiscal exposure to the taxpayer, giving democratic institutions clear visibility of the implications of multi-layered policy systems before decisions are taken.

The framework does not eliminate governance risk; rather it provides structured mechanisms through which risk can be identified, examined and corrected.

This approach reflects the principle of ‘defence-in-depth’ used in other high-reliability systems such as financial regulation, aviation safety and nuclear oversight. In such systems, multiple layers of monitoring and correction ensure that emerging problems are detected early rather than after institutional failure.

Within the GRACE architecture, the Gate Taxonomy provides the initial governance testing layer, while the E–S–V–Z control spine provides ongoing monitoring and reconciliation of risk, fiscal exposure, transparency signals and institutional accountability.

Together these mechanisms are designed to help ensure that complex policy systems remain not only lawful and operationally deliverable, but also visible, bounded and corrigible as cumulative pressures develop.

Demonstration Test Cases

The GRACE methodology is illustrated through a series of analytical test cases included within the Green Paper.

These test cases demonstrate how governance questions can be examined using the framework’s decision gates and reconciliation architecture. They are analytical tools designed to stress-test system design and governance visibility using publicly observable institutional patterns.

Test cases do not represent findings of fact or allegations regarding specific individuals or organisations.

Purpose of the Methodology

The objective of the GRACE methodology is to support transparent public decision-making by ensuring that complex policy systems remain:

- Legible to democratic institutions

- Bounded by fiscal and legal constraints

- Subject to independent scrutiny

- Capable of correction when assumptions fail

In this way, governance becomes a practical discipline rather than a rhetorical aspiration, allowing interconnected policy systems to remain intelligible, auditable and corrigible over time.

Because the methodology focuses on legality, fiscal exposure, operational deliverability and transparency, it can be applied wherever decisions involve the use of public funds or the exercise of public power, helping ensure that such decisions remain visible, accountable and subject to democratic scrutiny.

Governance Notes

The following governance notes illustrate how the GRACE methodology

can be applied to recurring governance challenges observed in modern

public policy systems.

GRACE Principles

The GRACE Framework does not dictate outcomes.

It requires that decisions be tested, challenged, and justified.

It requires that any taxpayer burden is clearly attributed, transparently justified, and subject to defined mechanisms of review and, where necessary, reversal.

The analysis draws on publicly available government and institutional datasets. Where inconsistencies, gaps, or differences in methodology arise across sources, these are treated as governance signals requiring reconciliation, attribution, and transparent interpretation within the GRACE framework.

The GRACE Framework provides a structured method for assessing governance, risk, fiscal exposure, and safeguarding considerations. It is designed as an analytical framework to support evaluation and discussion. It does not define outcomes, nor does it replace formal legal, policy, or operational processes. Users should interpret the framework as a tool for structured analysis rather than a prescriptive or determinative system.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Public policy is often presented through persuasive narratives. Policies may be described as humanitarian, economic, security-driven or efficiency-focused.

Yet the story told about a policy is not always the same as the system that is ultimately constructed.

This gap between policy narrative and system design is one of the most persistent causes of governance failure.

Narrative manipulation in public policy

Narratives can be constructed in many ways. Policy discussions may:

- select convenient data

- frame problems selectively

- exaggerate or minimise risks

- emphasise intentions rather than operational design.

These behaviours appear in many areas of public policy. The question is therefore not whether narratives can be manipulated, but whether governance systems contain mechanisms that allow such narratives to be tested against structural reality.

How the GRACE framework constrains narrative

The GRACE methodology introduces structured governance tests that policy systems must pass.

Democratic Consent Test (DCT) — Requires that authority, scope and cost be clearly defined.

Economic Case Gate (EG) — Requires transparent fiscal exposure, funding mechanisms and sustainability.

Implementation Gate (IG) — Requires evidence that the system can be delivered operationally.

Risk and Assurance Gate (RAG) — Requires defined risk triggers and escalation mechanisms.

These tests shift debate away from narrative persuasion and toward verifiable system design.

Transparency through the GRACE architecture

The GRACE control spine further constrains narrative manipulation through its reconciliation architecture:

Annex E — Risk Registers

Annex S — Fiscal Attribution

Annex V — Transparency Dashboards

Annex Z — Reconciliation and Accountability Mapping

These mechanisms create visibility for risk signals, fiscal exposure, operational performance and institutional responsibility. Transparency makes narrative manipulation easier to detect.

Reproducibility and governance testing

One of the strongest safeguards within the GRACE methodology is reproducibility. Any analyst, journalist, auditor or parliamentary committee can apply the same governance tests.

They can ask:

- Was authority clearly defined?

- Are fiscal assumptions credible?

- Is operational capacity realistic?

- Are risk triggers monitored?

If a policy narrative diverges from the system design, the inconsistency becomes visible.

Narrative substitution

A common governance failure occurs when the narrative surrounding a policy diverges from the system that is actually constructed. A policy may be presented as humanitarian, economic, security-driven or equality-focused, yet the operational structure may produce very different outcomes.

The GRACE methodology exposes this divergence by requiring policies to pass independent governance tests.

Governance insight

The GRACE framework shifts policy debate from narrative persuasion toward structural accountability.

Instead of asking: ‘Do we like the policy narrative?’

The framework asks: ‘Does the system actually work?’

Closing principle

Public systems should not rely on scandal to trigger oversight.

Oversight should be embedded in the design of the system itself.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Public governance systems are rarely designed with the intention of failing. Yet many systems repeatedly produce predictable problems.

When these failures occur, they are often explained through operational mistakes, funding constraints, or unforeseen circumstances.

However, a deeper cause frequently lies elsewhere: institutional incentives embedded within the system itself.

Understanding how institutional incentives shape system design is therefore essential when analysing governance failures.

Institutional incentives in complex systems

Public institutions operate within a framework of incentives that influence decision-making.

These incentives may include:

- political timelines

- budget constraints

- organisational boundaries

- reputational risk

- pressure to avoid short-term instability.

While policy objectives may remain constant, these incentives often shape how governance systems are designed and implemented.

Over time, this can produce systems that appear coherent but quietly accumulate structural weaknesses.

Incentives and system drift

Institutional incentives can cause governance systems to drift away from their original purpose.

Examples may include:

- shifting costs between departments rather than resolving underlying issues

- prioritising short-term stability over long-term sustainability

- delaying difficult decisions that carry political risk

- designing systems that minimise institutional exposure rather than maximise effectiveness.

In such environments, governance systems may appear stable while underlying risks continue to accumulate.

How GRACE reveals institutional distortions

The GRACE methodology helps expose these distortions by requiring policy systems to pass independent governance tests.

For example:

Economic Case Gate (EG)

Reveals fiscal incentives and hidden cost transfers.

Implementation Gate (IG)

Identifies gaps between policy ambition and operational capacity.

Risk and Assurance Gate (RAG)

Highlights risks that institutions may prefer not to emphasise.

Because these tests operate independently, institutional incentives cannot easily conceal structural weaknesses.

Structural accountability

Another important feature of the GRACE framework is the mapping of institutional responsibility.

Governance systems must identify:

- who authorises the policy

- who funds the system

- who delivers operational services

- who monitors risk

- who evaluates outcomes.

This mapping ensures that responsibility remains attributable throughout the lifecycle of the system.

Governance insight

Many governance failures do not arise from malicious intent or deliberate wrongdoing.

They emerge when institutional incentives gradually reshape system design.

Recognising these incentives is therefore essential when building governance systems that remain transparent, resilient and accountable.

Closing principle

Effective governance requires not only sound policy objectives, but also institutional structures that align incentives with system outcomes.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Many major governance failures become visible only after a public crisis or scandal. Inquiries, regulatory reviews and emergency reforms are often launched once the problem has already produced significant consequences.

This pattern raises an important governance question: why do oversight systems frequently activate only after failure becomes visible to the public?

The pattern of reactive oversight

In many governance systems, oversight mechanisms are activated reactively rather than proactively. Risk signals may exist long before a crisis emerges, but these signals often remain fragmented across institutions.

As a result, governance systems may appear stable while underlying risks continue to accumulate.

Why systems rely on scandal

There are several reasons why governance systems drift toward reactive oversight:

- institutional fragmentation

- unclear accountability structures

- dispersed operational responsibility

- weak transparency mechanisms

- reluctance to escalate emerging risks.

When responsibility is distributed across multiple institutions, early warnings may not trigger coordinated action.

Cumulative risk in complex systems

Complex governance systems rarely fail because of a single decision. More commonly, failures emerge when multiple policy decisions interact across legal, fiscal and operational domains.

When these cumulative risks remain invisible, institutions may assume that administrative capacity or fiscal resilience will absorb the pressure.

While the GRACE methodology is designed as a general governance framework, it can also be applied to real-world events in order to examine how institutional systems respond to emerging risks.

The following illustrative test case demonstrates how the GRACE decision gates and reconciliation architecture can be used to analyse governance questions arising from a major urban safety incident.

The purpose of this example is not to determine responsibility for any specific event. Rather, it illustrates how the methodology can be used to examine regulatory oversight, operational capacity, fiscal exposure and risk escalation mechanisms within complex public systems.

Test Case insight

| Illustrative Test Case — Urban Safety Regulation and Institutional Risk Signals A recent commercial building fire in central Glasgow which destroyed a historic structure and disrupted major transport infrastructure illustrates broader governance questions concerning regulatory oversight, inspection regimes and institutional risk monitoring. While the specific causes of any individual incident remain matters for investigation, events of this kind highlight how risks within complex urban systems may accumulate across regulatory, operational and institutional domains. The GRACE methodology allows such situations to be examined by analysing authority, fiscal exposure, operational capacity and risk escalation mechanisms within the governing system. Applying the GRACE Methodology Democratic Consent Test (DCT) The first governance question concerns authority and accountability. Urban safety regulation normally involves multiple institutions, including licensing authorities, building regulators, fire safety inspectors and local government bodies. The Democratic Consent Test asks whether the governing framework clearly defines which institutions hold responsibility for authorising commercial premises, conducting safety inspections and enforcing regulatory standards. Absolute Rights Gate (ARG) Public safety systems exist to protect life and physical security. The Absolute Rights Gate therefore asks whether the regulatory framework provides adequate safeguards to prevent foreseeable threats to public safety within high‑risk commercial premises. Economic Case Gate (EG) Major incidents can produce significant fiscal consequences. Emergency response costs, infrastructure disruption, rebuilding expenditure and economic losses to surrounding businesses may create financial exposure extending beyond the original premises. Implementation Gate (IG) Even well‑designed regulatory frameworks depend on operational capacity. The Implementation Gate examines whether institutions possess the resources, personnel and coordination mechanisms necessary to enforce safety standards effectively. Risk and Assurance Gate (RAG) Major incidents rarely occur without earlier warning signals. Risk indicators may include safety complaints, inspection failures, regulatory gaps or operational pressures within enforcement bodies. The Risk and Assurance Gate examines whether governance systems contain mechanisms capable of detecting and escalating such signals before they develop into larger failures. Value Assurance Review (VAR) Following a major incident, governance systems often undergo review. The Value Assurance Review asks whether lessons identified through post‑incident investigations are incorporated into regulatory frameworks in order to strengthen institutional resilience and prevent recurrence. Application of the GRACE Control Spine (E–S–V–Z) Beyond the gate analysis, the GRACE methodology also examines how governance signals are reconciled across institutional systems through the E–S–V–Z control spine. Annex E — Risk Register and Thresholds Risk registers may capture indicators such as inspection failures, regulatory gaps, safety complaints or operational pressures within enforcement bodies. These signals provide early warnings that may indicate growing systemic risk. Annex S — Fiscal Framework Major urban incidents can generate fiscal exposure beyond the immediate premises. Emergency response costs, infrastructure disruption, rebuilding expenditure and economic losses to surrounding businesses may create broader financial impacts that require transparent attribution. Annex V — Transparency and Publication Signals Transparency mechanisms, including regulatory disclosures, investigative reports and published dashboards, allow external observers to monitor institutional responses and evaluate whether governance systems are functioning effectively. Annex Z — Reconciliation and Institutional Accountability The reconciliation layer connects risk signals, fiscal exposure and operational performance across the relevant institutions. By mapping these signals together, governance systems can better identify where responsibility lies and where corrective action may be required. Financial Risk Allocation and Insurance Considerations Major incidents involving private premises also raise questions about the allocation of financial risk between property owners, insurers and the public sector. In cases where buildings are destroyed or severely damaged, insurance coverage may determine whether rebuilding costs are borne privately or whether wider economic consequences fall partly upon surrounding businesses and public infrastructure. Where the ownership structure of a building, the presence of insurance coverage or the solvency of the responsible entity are unclear, fiscal exposure may extend beyond the original premises. Emergency response, infrastructure disruption and wider economic losses can ultimately create indirect costs for local authorities, transport systems and taxpayers. Within the GRACE methodology, these questions form part of the broader analysis of fiscal attribution and institutional responsibility. The framework therefore examines not only how incidents occur, but also how financial consequences are distributed across private actors, insurers and public institutions. |

This illustrative test case demonstrates how the GRACE methodology can be used to examine institutional systems rather than individual events.

Major incidents often reveal how risks accumulate across regulatory, operational and fiscal domains within complex governance systems. By applying structured governance tests, the GRACE framework helps identify where institutional visibility, accountability or risk monitoring may require strengthening.

In this way, the methodology supports earlier detection of systemic vulnerabilities before they develop into large‑scale governance failures.

How GRACE addresses reactive governance

The GRACE framework introduces structured governance tests designed to make emerging risks visible earlier in the policy lifecycle.

Through mechanisms such as:

- governance gates

- risk registers

- fiscal attribution

- transparency dashboards

- reconciliation controls

GRACE creates structured visibility for institutional risks that might otherwise remain hidden.

Structural oversight

Rather than waiting for crisis-driven oversight, governance systems should embed monitoring and escalation mechanisms directly into system design.

This approach allows risks to be identified, examined and corrected before they develop into large-scale failures.

Governance insight

When oversight relies on scandal, governance becomes reactive and unpredictable. Effective governance systems instead require structures that make risks visible early and assign clear responsibility for responding to them.

Closing principle

Public systems should not rely on scandal to trigger oversight.

Oversight should be embedded in the design of the system itself.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Public policy debates frequently focus on visible programme costs, yet significant fiscal exposure can develop outside the immediate budget line of a policy.

When costs are distributed across multiple departments, agencies or levels of government, the true fiscal impact of a system can become difficult to see.

How fiscal exposure becomes hidden

Large public systems often involve several institutions responsible for different elements of delivery. This can lead to costs being distributed across multiple budgets.

Examples may include:

- operational costs carried by local authorities

- enforcement or compliance costs borne by separate agencies

- downstream service pressures on health, housing or justice systems

- administrative costs absorbed within existing departmental budgets.

Institutional incentives and cost diffusion

When fiscal exposure is distributed across institutions, decision-makers may see only part of the overall cost structure.

This fragmentation can produce what might be described as cost diffusion, where no single body has full visibility of the system-wide fiscal impact.

Why visibility matters

Without clear fiscal attribution, governance systems may underestimate the long-term sustainability of public programmes.

Costs that appear manageable within one department can accumulate across the wider system, placing pressure on public finances over time.

How GRACE addresses fiscal visibility

The GRACE framework addresses this challenge through structured fiscal analysis.

The Economic Case Gate requires transparent presentation of fiscal exposure, funding mechanisms and sustainability assumptions.

In addition, the GRACE control architecture introduces mechanisms for tracking system-wide cost signals.

| Illustrative Example — Charity Funding Proposal A charity may apply for public funding to deliver a social programme. While the proposal may be framed in humanitarian or community terms, structured governance analysis would examine the system design more closely. Applying the GRACE methodology would ask questions such as: DCT — Democratic Consent Test Who authorised the funding programme? What is the scope, cost and expected outcome? ARG — Authority & Responsibility Gate Which public body holds legal authority for the programme, and who is accountable for oversight, delivery assurance and expenditure control? EG — Economic Case Gate What is the total fiscal exposure of the programme? How is the funding structured and is it sustainable? IG — Implementation Gate Does the organisation possess the operational capacity to deliver the programme safely and effectively? RAG — Risk and Assurance Gate What monitoring mechanisms exist to detect safeguarding risks, financial mismanagement or delivery failure? VAR — Value Assurance Review Does the programme demonstrate measurable public value over time, and are evaluation mechanisms in place to confirm whether the intended outcomes are being achieved? Governance assurance and conflicts of interest Structured governance analysis also considers the incentive environment surrounding public expenditure. Where programmes involve public grants, advisory bodies, delivery partners or policy advocacy organisations, assurance should exist that both financial and non‑financial conflicts of interest have been appropriately identified and managed. This includes circumstances where individuals connected to funding decisions, programme oversight, or policy advice may also hold roles within organisations receiving public funding or influencing programme design. Such circumstances do not imply impropriety. However, good governance practice requires that systems are capable of demonstrating that potential conflicts — including institutional, professional, reputational or funding‑dependency incentives — have been transparently assessed and mitigated. Within the GRACE framework, these considerations are reconciled at system level through the publication, attribution and reconciliation mechanisms described in Section 21 and the E–S–V–Z control architecture. The purpose is not to attribute wrongdoing but to ensure that public expenditure occurs within an environment of demonstrable transparency and accountable governance. |

Within the GRACE architecture, these governance tests operate alongside the E–S–V–Z control spine, which connects risk registers, fiscal attribution, transparency dashboards and reconciliation controls across the lifecycle of a policy system.

Fiscal attribution and transparency

Through tools such as fiscal attribution frameworks and transparency dashboards, GRACE aims to make system-wide fiscal exposure visible to decision-makers.

This allows governance institutions to evaluate not only the direct cost of a policy, but also its broader financial implications.

Governance insight

Effective governance requires fiscal visibility. When costs become fragmented across institutions, policy debates may underestimate the true economic impact of public systems.

Closing principle

Transparent fiscal attribution helps ensure that public policy decisions remain sustainable and accountable over time.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Safeguarding frameworks are often supported by strong legal duties and professional standards. Yet despite these protections, safeguarding failures periodically emerge across complex public systems.

Understanding why such failures occur requires examining not only legal obligations, but also the institutional structures through which safeguarding responsibilities are delivered.

The structure of safeguarding systems

Safeguarding responsibilities are typically distributed across multiple institutions, including:

- local authorities

- health services

- enforcement agencies

- education providers

- regulatory and oversight bodies.

Each institution may carry specific statutory duties, yet safeguarding outcomes depend on how these responsibilities interact across the wider system.

Institutional fragmentation

When safeguarding responsibilities are distributed across multiple organisations, risk signals may emerge in one part of the system without triggering coordinated responses elsewhere.

This fragmentation can create situations where early warning indicators exist but are not aggregated into a clear picture of systemic risk.

Operational capacity and safeguarding risk

Safeguarding systems also depend on operational capacity, including trained personnel, clear reporting structures and effective coordination mechanisms.

Where operational capacity is constrained, safeguarding responsibilities may exist in law but remain difficult to implement consistently in practice.

How GRACE examines safeguarding systems

The GRACE framework allows safeguarding systems to be examined through structured governance tests.

For example:

- Democratic Consent Test — clarifies legal authority and institutional responsibility.

- Absolute Rights Gate — examines protection of non-derogable safeguarding rights.

- Economic Case Gate — examines whether safeguarding systems are supported by adequate and sustainable resources.

- Implementation Gate — evaluates operational capacity and coordination structures.

- Risk and Assurance Gate — identifies monitoring mechanisms and escalation pathways.

More detailed safeguarding test cases appear in Section 13 of the Green Paper

Structural safeguarding oversight

Applying structured governance analysis helps reveal whether safeguarding systems are supported by clear institutional responsibility, operational capacity and risk monitoring mechanisms.

Where these elements are unclear or fragmented, safeguarding risks may accumulate over time.

Governance insight

Safeguarding failures rarely arise from a single decision. More commonly they emerge when multiple institutions interact without clear coordination, visibility or accountability.

Closing principle

Effective safeguarding requires not only legal duties but governance systems that ensure risks are visible, responsibilities are clear and responses are coordinated.

A GRACE Framework governance note

Published March 2026 | Author: Andrew Young

Introduction

Public policy proposals are often evaluated on the basis of their objectives or intentions. However, an equally important question concerns whether a proposed system can actually be delivered in practice.

Operational capacity is therefore a central element of effective governance. A policy that cannot be implemented reliably risks creating instability, inefficiency or unintended consequences.

The gap between policy ambition and delivery

Governance systems frequently encounter a gap between policy ambition and operational delivery.

This gap can arise when:

- institutions lack sufficient personnel or expertise

- coordination mechanisms are unclear

- administrative processes are overly complex

- supporting infrastructure is insufficient.

In such cases, policy objectives may remain sound while the delivery system struggles to operate effectively.

Operational capacity in complex systems

Large public programmes often depend on cooperation between multiple institutions. Operational capacity therefore includes not only staffing and resources, but also coordination between agencies, information sharing and clear reporting structures.

When these elements are weak or fragmented, operational risk increases significantly.

How GRACE evaluates system feasibility

The GRACE framework evaluates operational feasibility through the Implementation Gate (IG).

This governance test asks whether:

- institutions possess the necessary operational capacity

- delivery responsibilities are clearly defined

- coordination mechanisms exist between participating bodies

- reporting and escalation processes are operational.

Operational visibility and risk monitoring

Operational feasibility also depends on the ability to monitor delivery risks as a system begins operating. Governance structures must therefore ensure that performance indicators, incident reporting and escalation procedures are clearly defined.

Governance insight

Policy success depends not only on sound objectives but also on the practical ability to deliver complex systems reliably over time.

Closing principle

Effective governance requires aligning policy ambition with operational capacity.